Machine Learning with AddiVortes: A Bayesian Alternative to BART

John Paul Gosling and Adam Stone

2026-07-29

Source:vignettes/introduction.Rmd

introduction.RmdThis vignette provides a comprehensive example of how to use the

AddiVortes package for machine learning regression tasks.

AddiVortes offers a Bayesian alternative to BART (Bayesian Additive

Regression Trees), using Voronoi tessellations for spatial partitioning.

We will walk through loading data, training a regression model, and

making predictions on a test set using this powerful non-parametric

Bayesian approach.

1. Loading the Package and Data

First, we load the AddiVortes package. For this example,

we will use the well-known Boston Housing dataset, included within this

package as Boston.

# Load the package

require(AddiVortes)

# Separate predictors (X) and the response variable (Y)

X_Boston <- as.matrix(Boston[, 1:13])

Y_Boston <- as.numeric(as.matrix(Boston[, 14]))2. Preparing the Data

To evaluate the model’s performance, we need to split the data into a training set and a testing set. We will use a standard 5/6 split for training and 1/6 for testing.

n <- length(Y_Boston)

# Set a seed for reproducibility

set.seed(1025)

# Create a training set containing 5/6 of the data

TrainSet <- sort(sample.int(n, 5 * n / 6))

# The remaining data will be our test set

TestSet <- setdiff(1:n, TrainSet)3. Training the Model

Now we can run the main AddiVortes function on our

training data. We will specify several parameters for the algorithm,

such as the number of iterations and trees.

# Run the AddiVortes algorithm on the training data

results <- AddiVortes(

y = Y_Boston[TrainSet],

x = X_Boston[TrainSet, ],

m = 200,

totalMCMCIter = 2000,

mcmcBurnIn = 200,

nu = 6,

q = 0.85,

k = 3,

sd = 0.8,

Omega = 3,

LambdaRate = 25,

InitialSigma = "Linear",

showProgress = FALSE

)4. Making Predictions and Evaluating Performance

With a trained model object, we can now make predictions on our unseen test data. We will then calculate the Root Mean Squared Error (RMSE) to see how well the model performed.

# Generate predictions on the test set

preds <- predict(results,

X_Boston[TestSet, ],

showProgress = FALSE

)

# The RMSE is contained in the results object

cat("In-Sample RMSE:", results$inSampleRmse, "\n")

#> In-Sample RMSE: 0.9235547

# Calculate the Root Mean Squared Error (RMSE) for the test set

rmse <- sqrt(mean((Y_Boston[TestSet] - preds)^2))

cat("Test Set RMSE:", rmse, "\n")

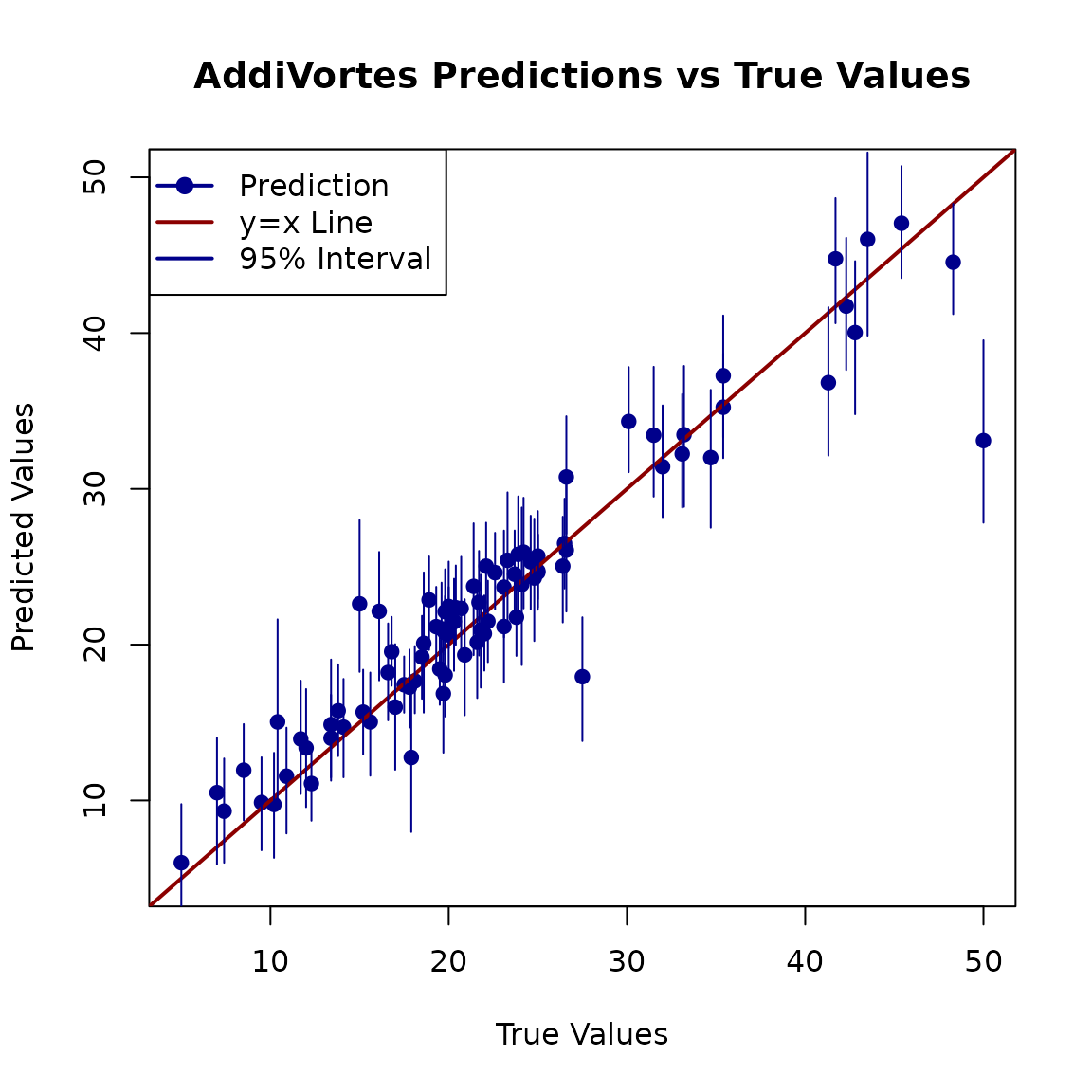

#> Test Set RMSE: 3.1729875. Visualising the Results

Finally, a good way to assess the model is to plot the predicted values against the true values. For a perfect model, all points would lie on the equality line (y = x). We will also plot the prediction intervals to visualise the model’s uncertainty.

# Plot true values vs. predicted values

plot(Y_Boston[TestSet],

preds,

xlab = "True Values",

ylab = "Predicted Values",

main = "AddiVortes Predictions vs True Values",

xlim = range(c(Y_Boston[TestSet], preds)),

ylim = range(c(Y_Boston[TestSet], preds)),

pch = 19, col = "darkblue"

)

# Add the line of equality (y = x) for reference

abline(a = 0, b = 1, col = "darkred", lwd = 2)

# Get quantile predictions to create error bars/intervals

preds_quantile <- predict(results,

X_Boston[TestSet, ],

"quantile",

showProgress = FALSE

)

# Add error segments for each prediction

for (i in seq_len(nrow(preds_quantile))) {

segments(Y_Boston[TestSet][i], preds_quantile[i, 1],

Y_Boston[TestSet][i], preds_quantile[i, 2],

col = "darkblue", lwd = 1

)

}

legend("topleft",

legend = c("Prediction", "y=x Line", "95% Interval"),

col = c("darkblue", "darkred", "darkblue"),

lty = 1, pch = c(19, NA, NA), lwd = 2

)